Play to Earn: Blockchain Gaming in Legal Focus

The concept of Play to Earn (P2E) describes a category of blockchain-based computer games featuring their own in-game economies. Players acquire digital assets, such as tokens or NFTs, through gameplay that hold real-world value. This model emerged in the late 2010s within blockchain gaming.

One early example was CryptoKitties (2017), a game famous for trading digital cats as Non-Fungible Tokens (NFTs). However, P2E gained significant attention in 2021 with titles like Axie Infinity, which rapidly attracted millions of players and generated high revenues. P2E games promised a revolution: players would no longer be mere consumers but true owners of their virtual goods, with the opportunity to earn money through gaming.

In developing countries, this was even promoted as a new income source. For instance, some players in the Philippines temporarily earned over 300 dollars a month with Axie Infinity, significantly more than the average local wage. For a lawyer specializing in blockchain law, this raises the critical question of whether these economic promises hold up to a legal reality check.

Economic Promises and Subsequent Disillusionment

The P2E model generated immense expectations. Proponents viewed it as a paradigm shift, allowing players to share in the financial success of games. “Play-to-earn blockchain games … could lead the way to a more equitable, opportunity-rich global economy,” enthusiasts declared during the 2021 crypto boom.

Players invested time and often money (for start-up capital like game tokens and NFTs) hoping to profit by reselling earned items or tokens. In low-income regions, P2E was particularly seen as an opportunity: thousands of Filipinos, for example, joined the trend and initially improved their living conditions. Simultaneously, investors poured capital into P2E start-ups, sensing a lucrative new business model, often referred to as GameFi.

A hype developed around virtual economies, with trading volumes reaching billions. Axie Infinity, for example, became the “most valuable NFT collection in the world” in 2021, with over 4 billion US dollars in trading volume.

Disillusionment Sets In

However, disillusionment has now emerged. Many P2E games proved unsustainable; players left or migrated, and token and NFT prices collapsed. Axie Infinity, for instance, lost over 90% of its market value and most of its users. Many who hoped for high returns now face empty wallets and disappointment.

One report stated: “Fourteen months later, most Filipino players … have exited the game nursing anger and anxiety – and, in some cases, thousands of dollars down.” This development challenges not only the business model but also the legal framework of P2E.

This article factually and legally examines how Play to Earn should be classified under German law. It addresses civil law (virtual goods, contracts), regulatory aspects (financial supervision, MiCAR), criminal and gambling law distinctions, and international perspectives (USA, Dubai). The aim is to highlight opportunities and risks for developers, start-ups, and players, assessing whether P2E is merely a temporary bubble or a sustainable model with a clean legal structure.

Technological Foundations of Play to Earn

To achieve a sound legal classification, the basic technical concepts of Play to Earn must first be understood. P2E games are inherently linked to blockchain technology and crypto assets. The most important elements include:

- Blockchain as Infrastructure: P2E games utilize distributed ledger networks (typically public blockchains like Ethereum or sidechains) to immutably document the ownership of game objects. Each in-game item or token is stored as a data record on the blockchain. This ensures transparency and prevents centralized manipulation of inventories, an advantage over traditional games where all data is held by the operator.

- Fungible Tokens: Almost all P2E games include at least one cryptocurrency, an in-game token. These fungible tokens serve as currency and rewards for achievements within the game. Examples are Smooth Love Potion (SLP) in Axie Infinity or VIS in Pegaxy. Such tokens can be generated in unlimited quantities (typically as gameplay rewards) and are often exchangeable for other cryptocurrencies or fiat money on exchanges. They form the economic basis of the game world (tokenomics). It is crucial that as soon as a token is freely tradable and has monetary value, it moves beyond pure gameplay and becomes subject to regulation. For more details, see our article on Security Tokens and Utility Tokens.

- Non-Fungible Tokens (NFTs): NFTs are unique, non-interchangeable tokens that typically represent game characters, virtual items, or properties. For instance, the creatures in Axie Infinity are implemented as NFTs. NFTs provide the player with a technically secured ownership right to the digital good. Players can hold, sell, or transfer the NFT in their own wallet without needing the game operator's permission. This creates a new form of ownership for virtual items; in traditional games, user contracts only grant a right of use, with the operator retaining full control. However, the legal ownership classification of NFTs is complex. While technically unique, they are not physical objects in legal terms.

- Gaming Ecosystem and Marketplaces: Central to P2E is an ecosystem allowing the trading of acquired tokens and NFTs. Developers often run their own marketplaces where players sell NFTs to others, with the operator earning fees. Many NFTs and tokens are also traded outside the game on general platforms (e.g., OpenSea for NFTs or Uniswap for tokens). This creates a secondary market where supply and demand dictate the price of in-game goods. Such markets require a certain degree of decentralization for the assets to be freely transferable. This distinguishes P2E from conventional games, where item trading is often forbidden or technically prevented to avoid gray markets and legal issues.

These technological foundations merge gaming with the real economy. Players' virtual successes can be directly monetized (“in-game items with real-world value”). Legal advisors must therefore consider both IT-specific aspects (smart contracts, decentralized structures) and financial market and media law implications.

Legal Classification in Germany

Several legal areas are relevant for the assessment of Play to Earn in Germany. P2E games transcend traditional categories by combining elements of digital services, financial products, and games. The following examines this phenomenon from the perspective of civil law, supervisory law, criminal law, and gambling law.

Civil Law: Contracts, Virtual Goods, and Property

Contractual Structures: A variety of contractual relationships exist within a P2E ecosystem. First, there's the user agreement between the player and the platform operator (game publisher), typically governed by general terms and conditions (GTCs). These define the conditions for using the game and the rights acquired over virtual goods. In traditional online games, GTCs usually state that all in-game items remain the property of the operator, granting the player only a limited right of use, an important mechanism for maintaining control.

With P2E, it might be argued that NFT technology grants players real ownership rights. However, this is legally complex under German law: only physical objects are considered property according to Section 90 of the German Civil Code (BGB). Virtual items or tokens lack physicality, making them not property in the property law sense; they are data or rights. Consequently, NFTs and game tokens primarily establish contractual positions—i.e., contractual claims or licenses of the player against the operator. The operator acknowledges the game object embodied in the NFT and enables its use in the game. Yet, they typically do not grant ownership in the BGB sense.

Trading Between Players: Another contractual relationship arises when players trade game items or tokens among themselves. For example, when player A sells an Axie NFT to player B. Legally, this constitutes a purchase agreement (Section 433 BGB) for a digital good. Even if an NFT isn't a "thing," sales law principles apply analogously to rights and other types of objects (Section 453 BGB). The seller owes the transfer of the token (by signing the blockchain transaction), and the buyer owes payment (often in crypto).

Nevertheless, such transactions differ from traditional purchases: they are not technically executed through physical transfer but via blockchain entry changes. Problems can arise where law and code diverge, such as in cases of bugs or hacking attacks. Who bears the risk if an NFT is "lost" due to a smart contract error? Such questions are largely unresolved in jurisprudence and would likely be addressed via general rules (e.g., tort law, duty of care). Courts might draw analogies to the purchase of digital products under contract law.

Property-Like Rights to NFTs: Some legal experts discuss whether an NFT could at least be considered intellectual property. Similar to a patent or share certificate, an NFT might be seen as a special sui generis right. However, no recognized legal basis for this exists yet. NFTs are neither legal tender nor traditional securities; they don't fit into traditional ownership categories. This is particularly relevant if a third party unlawfully "takes away" an NFT (e.g., by phishing a wallet). Without a physical object, there's no claim for return of property under Section 985 BGB. The injured party must resort to tort claims (data theft, Section 303a StGB, or fraud) and claims under enrichment law. In short: from a legal perspective, virtual goods are data and are protected primarily through contractual arrangements.

A well-drafted P2E contract should address this gap. For example, it should stipulate that NFTs are contractually assigned to the respective wallet holder, and the operator has no right of disposal without consent. This aligns with principles governing ownership of rights in game development.

GTCs and Control Mechanisms: The GTCs of P2E providers are a key instrument for managing legal risks. The operator can set rules for NFT trading (e.g., transaction fees, bans on off-exchange trades, exclusion of bot usage, etc.). Operators often reserve the right to block accounts or freeze assets in case of violations. However, decentralization presents an innovation here: Can an operator “confiscate” an NFT? Technically, no, as it's stored in the player's wallet. But the operator could block further game use, rendering the NFT worthless if it's no longer accepted in the game. Such clauses must be carefully and transparently formulated to be effective (Sections 305 et seq. BGB). Given the considerable values sometimes involved, ensuring fairness and a balance of interests is important, an area that will increasingly occupy consumer lawyers and courts.

Supervisory Law: Financial Instruments, Tokens, and MiCAR

A crucial question for P2E is whether and when issued tokens or operated marketplaces constitute financial instruments or financial services under supervisory law. In Germany, the German Banking Act (KWG) is especially relevant, supplemented by future European requirements like the Markets in Crypto-Assets Regulation (MiCAR).

Crypto Tokens as Financial Instruments: Since early 2020, German law has defined crypto assets as financial instruments in Section 1 (11) KWG. A crypto asset is a digital representation of value not issued by a central bank or public authority. It lacks legal currency status but is accepted as a medium of exchange or payment, or serves investment purposes, and is electronically transferable, storable, and tradable. This typically includes Bitcoin and Ethereum, but also game tokens if they are tradable beyond the game.

Example: The SLP token from Axie Infinity was traded on exchanges and held by players as an investment, thus meeting the criteria of a crypto asset (payment and investment function). As a financial instrument, crypto assets trigger various obligations: Anyone who trades, manages, or holds them for others operates a financial services business (e.g., crypto exchange or crypto custody) and requires a BaFin license. P2E platforms must therefore assess if their activities, e.g., as a multilateral trading system (marketplace for tokens/NFTs) or as an issuer of crypto tokens, require a license. This highlights the importance of understanding T&Cs, regulation & compliance in blockchain and computer games.

Classification under KWG and WpIG: In addition to the broad category of crypto assets, gaming tokens might fall under other classifications, such as units of account (Section 1 (11) sentence 1 no. 7 KWG) or securities. However, in most cases, the classic embodiment or investment structure is missing. BaFin has indicated broad standards: Anything resembling a means of payment or investment traded on the market can qualify as a financial instrument. For example, even simple gaming points were considered units of account if freely convertible. This means for P2E tokens: as soon as players invest real money to buy tokens or tokens can be exchanged for money, financial market law becomes relevant. A whitepaper or even a securities prospectus may then be required if there is a public offering component.

NFTs – Utility or Investment? The situation is somewhat different for NFTs. BaFin does not yet consider individual NFTs as financial instruments, provided they are unique and non-fungible. However, caution is advised: “NFTs may be considered financial instruments,” which creates regulatory uncertainty. For example, if an NFT is linked to continuous revenue rights (e.g., profit sharing in the game), it could be considered a security or investment. Purely game-related NFTs (skins, items) are more likely classified as digital consumer goods, where contractual terms apply rather than special financial market law. Nevertheless, if NFTs are traded on a large scale and used for speculation, supervisory authorities will closely monitor them. Future regulations for NFT platforms, possibly involving transparency obligations, are conceivable.

MiCAR – European Harmonization: The upcoming EU regulation Markets in Crypto-Assets (MiCAR) will provide uniform regulation for crypto assets in Europe from 2024/2025. MiCAR establishes an EU-wide framework for crypto assets, their issuers, and service providers. Essentially, MiCAR subjects all fungible tokens (except those already qualifying as financial instruments under MiFID) to certain rules. There are three categories: E-money tokens (stable value pegged to a fiat currency), asset-referenced tokens (stable by a basket of values), and all other crypto-assets, including so-called utility tokens.

A P2E game token like SLP would be a classic utility token, used for access and utility within the game. MiCAR will require issuers of such tokens to publish a detailed information document (Crypto Asset Whitepaper) and file it with the regulator prior to public offering. Unlike a securities prospectus, this does not require approval, but it mandates minimum content requirements and liability rules. For startups in the P2E sector, this means that issuing their own tokens publicly will become more formal and complex. However, MiCAR also creates legal certainty: what was previously a gray area will now be subject to clear, EU-wide rules. At the same time, crypto service providers (exchanges, custodians, advisors) will be subject to EU-wide authorization and supervision, enhancing consumer protection.

Transition and German Supervisory Law: National rules will continue to apply until MiCAR fully takes effect (parts from June 2024, the majority from end of 2024). In Germany, this means that even an NFT business potentially license-free under MiCAR could be subject to BaFin supervision until then. Crypto trading platforms for games, for example, currently remain subject to the KWG. P2E developers should carefully check the licensing thresholds: Does the company operate a platform for token exchange? It might be a trading system (Section 1 (1a) KWG). Does the provider store tokens/NFTs for players (e.g., in a custodial wallet)? This is a crypto custody business (Section 1 (1a) sentence 2 no. 6 KWG) and has been subject to authorization since 2020. BaFin has made it clear that it closely monitors crypto assets, and violations can lead to business prohibitions and criminal liability (Section 54 KWG). P2E start-ups are well advised to seek early legal advice and, if necessary, pursue a BaFin license or sandbox regulation instead of operating in a legal vacuum.

Criminal Law: Fraud, Pyramid Schemes, and Illegal Gambling

The criminal law aspects of Play to Earn are twofold. First, it must be determined whether fraudulent or pyramid scheme-like elements are present. Second, the question arises whether P2E could constitute illegal gambling if stakes and chance are involved.

Fraud Risks and Information Obligations: Many P2E projects aggressively advertise winning opportunities and high returns to attract new players (and their money). If these promises are objectively untrue or misleading, this could constitute fraud (Section 263 StGB). Fraud occurs when financial loss is caused by deception about facts. In P2E, this is conceivable: operators deceive about the sustainability of the business model (e.g., promising secure profits, although the system only works with constant user growth). Players might pay a high entry fee (NFT purchase) that is never recouped, with the money going to earlier players or operators. This blurs the lines with a Ponzi scheme.

Some critics openly call P2E a pyramid scheme: “New players pay the profits of old players … Adele Spitzeder and Charles Ponzi send their regards.” Indeed, purely profit-driven P2E games are often economically zero-sum games, where only redistribution occurs without external added value. This becomes criminally relevant when a system operates by design, functioning only through a constant influx of new funds, and the initiators conceal the true risks. While German criminal law lacks a specific "snowball paragraph," such structures are sanctioned via fraud or prohibited pyramid schemes under the Unfair Competition Act.

Ponzi Scheme vs. Legitimate Game: The distinguishing criterion is whether the game offers intrinsic added value (fun, entertainment) or if participation is primarily for profit expectation. If the game provides genuine enjoyment and players could theoretically enjoy it without earning money, it argues against a pure pyramid scheme. In such a case, a lack of new players would affect the economy, but the game wouldn't immediately collapse, as a core of players would remain for fun. However, if the entire model is structured around new payers enriching existing ones, it strongly suggests a fraudulent system. The prosecution must then examine whether deception occurred, for example, regarding success prospects. A poor business model isn't punishable per se, but intentionally creating an impression of investment security (e.g., “the money works for you”) can raise suspicion.

Unlawful Gambling: Another criminal law dimension involves gambling law (Sections 284, 285 StGB). Section 3 GlüStV 2021 defines gambling as a game where a fee is charged for a chance to win, and the outcome depends predominantly on chance. Classic P2E games are initially games of skill, requiring players to fight, collect, and trade. However, random elements often exist, such as loot box openings or random NFT generation (e.g., breeding in Axie Infinity, where offspring have random properties).

Section 284 StGB becomes relevant when players place bets to obtain a real chance of winning by chance. Some P2E models require buying “loot boxes” or boosters that randomly contain NFTs of varying value. This mechanism closely resembles a gambling machine (stake vs. random win). If such processes occur without official permission, the operator could be prosecuted for the unauthorized organization of a game of chance. The legal debate is controversial whether loot boxes in games are already games of chance. So far, German authorities have tended not to classify loot boxes as gambling under the GlüStV, as long as the prize is only virtual and no direct monetary value is paid out. With P2E, however, virtual winnings do have monetary value (being tradable), increasing the risk of being considered gambling.

Differentiation and Eligibility: Not every P2E is automatically a game of chance. If the main influence on winning is player performance (skill) rather than chance, it's more an e-sport or game of skill (not covered by GlüStV). Furthermore, a classic "stake" is often absent: many P2E games can technically be played for free; NFT investment is voluntary for faster progress. In practice, however, initial purchases are often necessary for effective play, which can be seen as a stake. Example: Starting Axie Infinity required owning three Axie NFTs, which at times cost a three-digit dollar amount. This purchase is functionally comparable to a wager to gain a chance to win. If the game then includes random mechanisms (e.g., randomized battle results or breeding luck), it dangerously approaches gambling.

The legal consequences of illegal gambling are severe: the organizer faces prosecution under Section 284 StGB (up to 2 years imprisonment), participants under Section 285 StGB (up to 6 months). Regulatory measures also loom; the Joint Gaming Authority (GGL) can block websites and payments. A P2E provider would need a German gambling license, which became possible in 2021 for online poker and virtual slot machines. However, requirements are strict (EU domicile, minor protection, addiction prevention, stake limits, etc.), and it's questionable if a P2E game could fit this framework. Conclusion on criminal law: Developers should design P2E mechanics to avoid illegal gambling. This means optional random reward design without compulsory payment, or a clear positioning as a game of skill. Marketing and promises must also be honest to avoid fraud. Otherwise, they operate in high-risk legal territory with personal criminal liability for those responsible.

Assessment Under Gambling Law (Section 3 GlüStV)

Gambling supervisory law is closely linked to criminal law. The Interstate Treaty on Gambling (GlüStV 2021) regulates which games are eligible for licensing. P2E models are new territory here and must be checked against the GlüStV's definition and system.

Concept of Gambling: As mentioned, gambling occurs when a fee is paid for a chance of winning, and the prize depends on chance. Applied to P2E, this means: Does the game directly or indirectly require money or valuable tokens for an uncertain chance of winning? A pure grinder, where players earn tokens through diligence, wouldn't be gambling, as there's no stake for a specific chance, but rather continuous performance. However, mechanisms like loot boxes, gacha pulls, or random NFT mints for a fee are critical. If, for instance, players receive a surprise NFT for 10 tokens, whose value depends on chance, it closely resembles gambling (comparable to a lottery). In traditional games, it was argued that the prize was "only" virtual. But as soon as NFTs/tokens are tradable on the market, this profit represents real value, blurring the distinction between virtual and real. There is therefore a real risk that P2E with such elements could constitute illegal online gambling in the authorities' view.

Loot Box Comparison: Loot boxes in video games have sparked controversial international debates. Countries like Belgium and the Netherlands have banned them as illegal gambling if purchased with real money. In Germany, there is no explicit ban yet; the focus is more on protecting minors through higher USK/FSK ratings for loot box games. For P2E, however, if a random-based reward is linked to a financial stake, it falls at least into a gray area. In doubt, the GGL would require a permit, which doesn't exist for such novel mechanics, as licenses are only issued for defined offers (sports betting, online casino, slot machines). P2E doesn't fit existing categories. The only option is to avoid such chance-based pay-to-win elements or design them without stakes. This also relates to broader concerns about age verification on the internet for providers.

GlüStV Conformity Check: A P2E provider must analyze its game to determine if the user receives a paid opportunity to participate in a chance-determined outcome. If so, the game may be classified as gambling. Even if player performance (skill) influences the outcome, a predominantly random factor is sufficient. If unclear, authorities could demand an expert opinion or temporarily prohibit the offer. Example: A game distributes NFTs as quest rewards, but which NFT (rare vs. common) is received is randomized. If players had to buy expensive equipment for this quest (with value), a stake/gain structure exists.

From the provider's perspective, it's advisable to contact the gambling supervisory authority early. If necessary, seek exemptions or, if the model allows, an official license in a less regulated EU country (Malta, Gibraltar) and rely on geoblocking in Germany. However, this contradicts the claim of a globally open game. Until legislation provides clearer guidelines, P2E models face a latent risk of being classified as illegal gambling and banned.

In summary, Germany presents a challenging legal environment for Play to Earn. Financial and gambling regulators tend to adopt a restrictive approach to ensure consumer protection, minor protection, and financial market stability. Many P2E projects are therefore set up abroad, a topic further explored in the next section.

International Perspectives

The legal treatment of Play to Earn varies significantly by jurisdiction. A comparison with the USA and Dubai (as part of the Crypto Oasis) reveals differences crucial for choosing a location for P2E start-ups.

USA: SEC and Howey Test – Are P2E Tokens Securities?

In the United States, crypto projects are primarily subject to securities law. The U.S. Securities and Exchange Commission (SEC) has long examined token models to determine if they are unregistered securities. The benchmark is the Supreme Court's famous Howey test: an investment contract (and thus a security) exists if (1) money is invested in (2) a common enterprise, (3) with an expectation of profit (4) substantially through the performance of others. The SEC has affirmed these criteria apply to gaming tokens.

In practice, the first two points are almost always met: anyone buying tokens or investing effort makes a commitment, and online games constitute a joint project. Points 3 and 4 are controversial: does the player expect profit from the efforts of others? In many P2Es, this is precisely the case. Players buy in-game currency/NFTs expecting future profit from value appreciation, which depends on the game's success (i.e., developer work). This often means the token fulfills the Howey criteria and is considered an investment contract, hence a security.

The consequence: Offering unregistered securities is illegal, according to the SEC. Developers selling in-game tokens or NFTs risk enforcement actions. The SEC can issue injunctions, penalties, and order repayment of investor funds. Since 2018, the SEC has warned that many utility tokens are in fact securities. Recently, it has intensified actions against crypto projects (e.g., SEC v. LBRY, SEC v. Ripple), though court classifications haven't always been clear. For P2E, even if a token's primary use is gaming, it can be a security if marketing or tokenomics imply profit promises. Example: Developers advertise the token as an investment or retain a share to increase its value—this might suffice for Howey's expectation.

However, counterexamples exist: if a game token is purely an in-game currency, not publicly advertised for sale, and players earn it solely by playing (and perhaps trading on third-party exchanges), it could be argued there's no investment of money with the developer. Some crypto games in the US attempt this route: tokens are not sold directly but only earned in-game, with the market created secondarily. They aim to avoid securities law. Yet, the SEC scrutinizes such cases, especially if developers indirectly profit from trading or award initial tokens to specific groups.

Differences to Germany: In the USA, crypto regulation is principle-oriented and shaped by common law courts. The Howey test is flexible and covers much that might slip through in Germany due to a lack of legal definition. For example, the US doesn't require a specific list like the KWG; investment contract is an open term. On the other hand, less discussion occurs about gambling beyond securities, as it's separately regulated at the state level. A P2E game with gambling mechanics might even be licensed in Las Vegas, while completely illegal in Germany.

Tax law also differs: players' profits are taxable income in the USA (regardless of holding period), whereas in Germany, private token sales could be tax-free after one year. However, given the complexity, we'll omit tax issues here.

In summary, P2E developers in the US market must especially ensure they don't sell unregistered securities. Close coordination with US attorneys and, if necessary, no-action letters from the SEC (a type of clearance certificate) are advisable for targeting American users. The risk of class-action lawsuits from dissatisfied players (who see themselves as investors) for false promises or rule violations is also real, given the US legal culture's greater propensity for litigation.

Dubai and the Crypto Oasis: Regulation in a Sandbox Paradise?

While Western countries often have strict or unclear regulations, the Dubai/United Arab Emirates region actively courts crypto and blockchain companies. The term Crypto Oasis signifies a flourishing ecosystem in Dubai, Abu Dhabi, and the surrounding areas that attracts numerous start-ups. What makes Dubai attractive?

First, the tax climate: Dubai levies no income or capital gains tax on crypto profits. Investors and players can realize profits tax-free (though foreign investors remain subject to their home country taxes; US citizens are taxed globally). This tax advantage is part of the appeal but not the sole factor.

The regulatory approach is more decisive: Dubai established its own supervisory authority for virtual assets in 2022, the Virtual Assets Regulatory Authority (VARA). VARA issues rules and licenses to crypto companies in Dubai (outside the DIFC financial center, where the DFSA is responsible). The philosophy is considered “progressive and responsive,” aiming to establish Dubai as a global crypto hub. VARA indeed offers clear regulations and appears to collaborate more closely with the industry than many Western regulators. For example, Dubai has special free zones like DMCC Crypto Centre or the newer RAK Digital Assets Oasis, which promise simplified licenses for crypto companies. The latter even boasts being the world's first unregulated free zone for Web3 companies, though this doesn't mean complete regulatory freedom; companies must still comply with certain UAE standards. This proactive approach contrasts with the often complex legal grey areas that startups face elsewhere.

Dubai offers the following advantages for Play to Earn start-ups:

- Licensing and Sandbox: VARA regulates activities requiring licenses (e.g., exchange operations, custody, token issuance). Startups can obtain a provisional license comparatively quickly and test their model in a sandbox environment. Authorities seem willing to approve innovative models if basic consumer and AML requirements are met. For instance, Crypto.com received a VARA license in 2023 for crypto services. A P2E game would likely be classified, if at all, as a virtual asset service, regulatable in Dubai, whereas in Germany, a suitable license category might not exist (or entail enormous effort).

- Clarity on AML/KYC: The UAE has clear anti-money laundering regulations for the crypto sector. Companies must comply with strict KYC standards, submit SARs (Suspicious Activity Reports), and implement the FATF Travel Rule. This may sound stringent, but it provides a clear framework. Similar rules apply in Germany (GwG), but in Dubai, practical implementation seems easier for crypto companies due to close authority support. However, AML is generally challenging for P2E, with many micro-transactions, regardless of location.

- No Gambling Blockade: The UAE traditionally has restrictive gambling laws (culturally), but video game loot boxes are less regulated there, with a focus on crypto. A P2E game could potentially operate its mechanics as "crypto-asset entertainment." However, the UAE is also launching a regulatory push for online gambling in 2023, so caution is advised.

- Infrastructure and Capital: Dubai offers access to well-funded investors and a growing community of blockchain developers. Many Asian P2E gaming companies have relocated to Dubai or Abu Dhabi for the friendlier climate. Hundreds of companies reportedly moved to the Emirates following China's crypto ban in 2021 (“blockchain startups in droves”).

However, there's a downside: Market access to the EU/USA could suffer if regulated exclusively in Dubai, as European regulators don't accept Dubai licenses as substitutes for their requirements. Furthermore, ongoing compliance costs in the UAE are not trivial (high license fees, local sponsor requirements, etc.). Nevertheless, Dubai is a serious alternative for the location choice of many P2E projects. One can operate within an internationally recognized framework, enjoy tax exemptions, and relative regulatory leniency as long as no obvious violations occur.

Choice of Location vs. Germany: A P2E startup in Germany faces complex legal issues, uncertain approval chances, and potential prohibitions. In Dubai, it's welcomed if it registers and complies with standards. This dichotomy means Germany often remains a bystander in new blockchain gaming trends, while innovation happens elsewhere. From a legal expert's viewpoint, clients should be honestly informed: it might be more sensible to initially set up operations abroad and later, once the model is consolidated and EU regulations clearer (e.g., MiCAR), expand to Germany.

Economic and Moral Considerations

Beyond strict legal analysis, it's important to consider the economic realities and ethical implications of Play to Earn. Legal advice must integrate these aspects to protect clients from misconceptions. This is often why traditional game developers are skeptical of P2E.

Unfulfilled Promises and ROI Errors

As outlined earlier, P2E ultimately caused losses for many players. Initially, the promise of return on investment (ROI) was sometimes enormous; players were suddenly seen as investors. However, the system often only worked during the upswing. Early entrants profited by selling acquired NFTs to later entrants, who then sold to even later entrants. As user growth stagnated, the cycle broke: NFT prices plummeted, leaving the last buyers with worthless "assets."

Take Axie Infinity: an Axie cost a few dollars in 2020, peaked at USD 2,000 during the 2021 hype, but crashed in 2022. Many players invested large sums (sometimes on credit), expecting steady returns, only to suffer massive losses. This late investor problem resembles financial bubbles, raising the moral question of operator responsibility. Did they provide transparent risk information? Or actively foster the illusion of playful money printing?

Tilman Baumgärtel accurately wrote in the taz that Axie Infinity was “actually just a visual interface for generating a cryptocurrency”, allowing players from the global North to profit from poverty in the South. This drastic description as digital feudalism highlights a moral issue: many P2E games exploit the hopes of poor populations, with wealth ultimately concentrating among a few profiteers. This raises ethical issues and liability risks inherent in complex systems.

Gamers as Investors

The traditional gamer plays for fun and spends money on entertainment. In P2E, they become investors aiming to earn money. This shifts the entire structure: where frustration over a bad game was once emotional, it's now financial. Players make investment decisions (buying NFTs) and become speculators. Psychologically, this can be toxic. Reports describe formerly enthusiastic Axie players lamenting that the game became a stressful chore to avoid losing money. Joy gave way to compulsion, similar to gambling addicts trying to recoup losses. Legally, the question arises whether game manufacturers have a special duty of care towards such “investor players.” For example, should they issue risk warnings as for financial products? This would be new but is under discussion. In any case, a provider's reputation suffers if players are financially ruined.

A moral assessment often concludes that pure play-to-earn, which only retains players for money, is problematic. The industry recognizes this, emphasizing play-and-earn, where game enjoyment takes precedence, and earning is secondary. This approach can be seen in discussions about contractual framework for live service games.

Developers' Interests: Why Major Studios Shy Away from P2E

Established game publishers (EA, Activision, Ubisoft, etc.) have been hesitant with NFT/P2E initiatives. Ubisoft launched its Quartz program with NFT items for Ghost Recon in 2021 but faced massive player backlash and soon halted the project. Valve (Steam's operator) banned blockchain games from its platform, stating it doesn't allow items with real-world value. The reasons for this reluctance are complex:

- Firstly, legal uncertainty: no major studio wants to risk suddenly being classified as a financial service provider or gambling operator.

- Secondly, brand and reputation protection: the gaming community currently reacts negatively to NFTs and "moneymaking" in games. Companies fear backlash and boycotts of their established franchises.

- Thirdly, economic cannibalization: traditional free-to-play models thrive on players constantly spending money (skins, loot boxes) without payout. P2E flips this: players want to extract money. This threatens the business model or demands entirely new revenue streams (e.g., higher initial sales, transaction fees). Many developers don't yet see a sustainable monetization plan where P2E is superior.

- There are also legal obligations: a studio issuing NFTs would need to ensure their long-term availability. What if servers shut down in 5 years? Could NFT owners sue because their asset becomes unusable in the game? Such questions are daunting. This is related to the broader topic of establishing a clean chain of rights in game development.

Finally, ethical responsibility plays a role. There's an industry debate whether enticing players to “work in the game” is desirable. Critics warn of exploitation risks if wealthy players set up scholar programs where poor players "grind" for them (observed in Axie). This feels like colonialism 2.0 and clashes with many developers' self-image, who aim to deliver entertainment and artistic vision, not just financial products.

Decentralization vs. Platform Control

Another aspect is control over virtual goods. P2E promises decentralization: players own assets and trade them freely. However, this undermines platform control over its ecosystem. Traditional providers argue they must control the in-game economy for balance and gaming experience. If items are traded externally en masse, black markets and fraud can flourish, problems known before blockchain (e.g., skin gambling with CS:GO skins). Blockchain makes the market more transparent but no less real; now anyone can track in-game item values and trade them like stocks. For a development studio, this means losing some ability to design item flows due to external prices and speculation. The studio may also lose revenue: in a closed system, the operator profits from every item sale (e.g., loot box purchase). In an open system, players trade among themselves, and without royalty mechanisms in smart contracts, the studio gains nothing. This is why many P2E games come from new companies experimenting, while major players wait or only test symbolic NFTs (without gameplay influence).

In summary, lofty P2E promises have not yet been fulfilled economically; instead, models' fragility has become apparent. Morally, P2E concepts face criticism for turning fun into capitalist competition where most ultimately lose. These insights now inform legal advice: a lawyer must advise clients that a legally compliant P2E model faces not only legal hurdles but also fundamental economic doubts. Sustainability, fairness, and transparency should guide such projects for success. This is also why we emphasize blockchain technology in rights management.

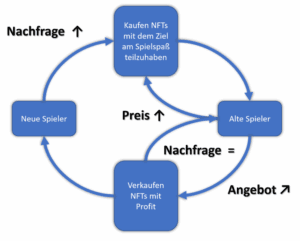

Diagram of a sustainable play-to-earn economy (upswing phase): The diagram illustrates the cycle in a P2E game. New players join and buy NFTs (e.g., game pieces), which increases demand and the price of existing NFTs. Old players can then sell their upgraded NFTs at a profit. As long as new players continuously join (demand ⬆️), the system remains balanced. Players receive monetary incentives alongside entertainment.

It becomes problematic when user growth slows (demand ⬇️). If newcomers stop joining, there's no fresh money for older players, NFT prices fall rapidly, many players leave in panic, and the system collapses. A sustainable P2E model must therefore ensure that value isn't merely redistributed from new to old users. Instead, real value must be created by the game (e.g., through external revenue or long-term motivation independent of profit).

Legal Risks for Developers and Start-ups

Given the points outlined above, the considerable legal risks associated with P2E are understandable. Developers and startup founders must be aware of numerous pitfalls to avoid costly legal disputes or regulatory actions. The most important risk areas include:

Licensing and Reporting Obligations (BaFin, GwG)

A key risk lies in conducting financial market-related transactions without necessary authorization. As explained, P2E tokens and marketplaces can qualify as financial instruments or services. Providing such services without a BaFin license is illegal and can lead to business bans and criminal proceedings (Section 54 KWG). Startups must proactively assess whether, for example, a license as a crypto custodian, proprietary trader (if they trade tokens themselves), or operator of a multilateral trading system is required.

Applying for a license is time-consuming and costly, but often indispensable for operation. One strategy is to design the business model to stay below thresholds, e.g., by not offering custodial services (non-custodial wallets) or selling tokens via third-party platforms. However, such constructions are not always sufficient, and MiCAR will close many previous loopholes. This is a common concern addressed in blockchain startups and new regulations.

Money laundering obligations (GwG) also apply. If a P2E provider is considered an obligated party (typically for crypto services), it must, among other things, identify customers (KYC), submit suspicious activity reports (SARs) for suspected money laundering, and implement internal security measures. Sections 10 and 11 of the AMLA require full user identification above certain transaction volumes and reporting unusual transactions to the FIU. In practice, this means that if players trade tokens for fiat or withdraw large sums, their identity must be known and verified. This is a significant hurdle for a global online game; anonymous crypto transactions are then no longer permitted. Some P2E platforms therefore limit payouts (e.g., only after KYC up to an amount of X per month). Note: AMLA obligations apply regardless of a BaFin license. Anyone operating without a license can still be an "anti-money laundering obligated person," for example, as a trading platform operator for crypto assets. Violations of AMLA (e.g., no KYC, no money laundering officer) can result in multi-million Euro fines.

Civil Liability Risks

Various liability issues arise in P2E projects: Is the operator liable if players suffer financial losses? Generally, providers attempt to exclude or limit liability in their general terms and conditions, especially for lost profits or loss of value of tokens/NFTs. However, not every clause withstands GTC scrutiny, particularly concerning consumers. For example, if an operator grossly neglects security, leading to a hack (as with the Axie Ronin network in 2022, where over $600 million was stolen), it could be liable for damages if organizational negligence is proven. Players could argue the provider promised to keep assets safe, which would constitute a breach of secondary contractual obligations.

System failures or game termination also raise questions: if a game is discontinued, what happens to invested values? In traditional games, virtual items become worthless, accepted by users as they have no ownership. In P2E with NFTs, it's different: NFTs persist, but without the game, they are de facto useless. Could players claim damages because the promised ecosystem disappeared? This would depend on whether the operator contractually guaranteed continued provision. Most GTCs exclude this ("no claim to game availability"). However, such clauses could be invalid if the business model implicitly aimed for long-term operation. This is uncharted legal territory, but courts might rule for consumers in cases of blatant value decline, e.g., via frustrated business bases (Section 313 BGB). This parallels discussions around the right of withdrawal for NFT purchases.

Liability in Player-to-Player Trading: Platform operators could also be involved in user-to-user transactions. For example, if a marketplace trade fails (e.g., NFT not delivered due to a bug). This raises whether the operator is liable as an intermediary. Terms and conditions often exclude liability for user trades, with the operator seeing itself only as a technical service provider. Nevertheless, it could be liable as an indirect tortfeasor if, for instance, fraud occurs via its platform and it fails to intervene. There's an analogy with auction platforms: eBay had to intervene in certain circumstances to prevent infringements once aware. Thus, if fraudulent offers appear on the P2E marketplace (phishing links, etc.), the operator must react, or risk claims from injured users. This highlights aspects of liability of website operators for user content.

Furthermore, consumer protection rights must not be overlooked. For example, the right of withdrawal in distance selling: if a user buys an NFT in the operator's store, this is a digital product. According to Section 312f BGB, the right of withdrawal for digital content lapses upon execution, but formalities (information, consumer consent to lapse of withdrawal right) must be correct. If the provider fails, a player could cancel an NFT purchase, problematic if the NFT has been resold or consumed.

Finally, there's a latent risk of tortious liability: if the P2E game appeals to children or young people, and they are deliberately tempted to play excessively due to earning potential, it could be examined whether this constitutes immoral intentional damage (Section 826 BGB). While theoretical, discussions about loot boxes and young players show that moral and ethical boundaries are relevant. Companies should implement minor protection mechanisms (age verification, limits for under 18s).

Problematic Contract Design and GTC Pitfalls

As mentioned, the terms and conditions and user agreements of a P2E game form the legal backbone of the offer. Numerous traps lurk here:

- Ownership and Usage Rights Clauses: It must be clearly regulated what exactly the player acquires when buying an NFT. Do they only have the token or also a right to use the underlying character/image? What about copyrights (e.g., if a player creates or reuses NFT assets)? Unclear clauses could lead to disputes or invalidity. Ideally, the player should be granted a simple right to use the content for as long as they hold the NFT, defining what they are (not) allowed to do with it. This involves complex considerations of blockchain technology in rights management.

- Fees and Currencies: Many P2E games use their own tokens as currency. The terms and conditions should state these have no fixed value, are subject to fluctuations, and there is no promise of conversion back into fiat (unless explicitly offered). Convertibility is particularly tricky: if the operator promises, "You can cash out your tokens for real money at any time," this could be a financial service (bureau de change) for regulatory purposes. It's better to state: "Tokens can be traded on third-party platforms; the operator itself does not exchange." Transaction fees (e.g., % for NFT trading) must also be transparently stated, or risk warnings for lack of transparency.

- GTC Control: Consumer GTCs are subject to strict control under §§ 307 ff. BGB. Clauses excluding liability for intent/criminality are invalid. The same applies to clauses unilaterally granting extreme rights to the operator (e.g., deleting assets at any time without cause). Numerous judgments in classic games already exist on account suspensions. P2E providers should specify important reasons for sanctions (cheating, payment fraud, hacking, etc.) and maintain proportionality. NFTs are complex: if a user is banned, their NFT becomes worthless in-game—effectively an expropriation. Such consequences should be openly communicated, and compensation possibly provided (e.g., warning levels instead of immediate bans).

- Choice of Law and Jurisdiction: P2E start-ups often base themselves abroad but serve German customers. GTCs then attempt to specify foreign law (e.g., Singapore law) and offshore jurisdiction. However, this may be ineffective for EU consumers, who enjoy mandatory protection of their home country and can sue at their place of residence. This means even a foreign company could be sued under German law. Risk management should account for this eventuality and not blindly rely on exotic legal clauses.

Further Duties: Data Protection, Protection of Minors, Tax

Aside from major issues, other legal obligations exist. Data protection (GDPR) is relevant for P2E, especially with KYC and tracked financial transactions. An EU provider must be GDPR-compliant, e.g., provide information on data processing, obtain consent (e.g., if blockchain transaction IDs are published, potentially personal). Protection of minors: If the game contains 18+ elements (e.g., gambling-like or monetary losses), it must not be freely accessible to young people. In Germany, state media authorities could classify a P2E game as “developmentally harmful” and require age verification. Start-ups should consider a USK/PEGI rating and, if in doubt, only offer the game from age 18 for safety, though this limits the user base. This reinforces the need for robust data protection strategies.

There are tax risks for both operators (VAT on commissions, income tax on winnings) and players (income tax on gaming revenue). Tax authorities may consider intensive P2E a commercial activity for players, with corresponding trade registration obligations. This area holds much potential, but in-depth analysis is beyond this article's scope. Importantly, even if P2E operates in a legal gray area, it doesn't exempt companies or users from fulfilling tax obligations.

Outlook: Future of Play to Earn – Bubble or Game Changer?

After the boom and bust of the first generation of Play to Earn, the question arises: is the trend already over, or are we experiencing an evolution toward sustainable models? Some developments are foreseeable, both legally and economically.

Regulatory Clarity on the Rise

With MiCAR in Europe and clearer SEC requirements in the US, the legal framework will consolidate from 2024/25. This may increase hurdles (due to regulating many P2E tokens) but also enhance credibility. Projects achieving compliance will be perceived as more trustworthy. BaFin-regulated or VARA-licensed games could become a quality seal, assuring players against fraud. Special license categories for play-and-earn might also emerge, e.g., in media or gambling law, if pressure to contain such offers increases.

Shift to Play-and-Earn

According to the community and industry, the future lies in play-and-earn rather than play-to-earn. This means games should primarily be fun and retain a loyal community; earning money is an accessory, not the core purpose. Such games could have smaller, legal in-game economies (e.g., tradable cosmetic NFTs) without the full-blown financial incentive system of early P2E. For lawyers, this means less risk, as virtual goods can be traded as before, just on the blockchain. One trend is soulbound tokens (non-tradable performance NFTs), documenting successes without speculation, which could replace reward systems without provoking legal issues like securities status.

Integration into Existing Games

Perhaps we will see fewer purebred P2E games, but elements of it in major titles. Some studios consider outsourcing parts of their in-game economy to blockchain (e.g., officially allowing item trading between players, but with gameplay as the main element). If such hybrid models emerge, they will certainly undergo legal scrutiny and conservative design to avoid regulatory conflicts. This is particularly relevant for IT contract law for startups.

New Business Models

One legally interesting concept is move-to-earn (players earn tokens for physical activity) or learn-to-earn (educational games with token rewards). This blurs boundaries with loyalty programs. Legally, such tokens could be considered reward points redeemable for a limited time, similar to loyalty programs like Payback. Such models are usually uncritical as long as the token isn't freely convertible. Perhaps one way forward is to design P2E tokens as a closed-loop currency (only usable in the game or with partners, no official secondary market). While reducing attractiveness for pure “earners,” it could be legally simpler and still provide incentives.

Bubble Burst, But...

Many experts consider the big P2E hype a bubble that burst in 2021. User numbers and token market capitalizations support this. However, the idea of giving players real assets has resonated. In a toned-down form—e.g., digital ownership of purchased skins—this is likely to remain. The challenge will be to develop legally clean models that create value rather than just shifting it. For example, future games could be ad-financed and distribute part of the revenue to players as crypto (play and earn without new players having to pay). This would be sustainable as long as advertising money flows. Legally, clear contracts would be needed regarding revenue distribution, avoiding Ponzi schemes. Cooperation with brands (NFTs as fan merchandise in-game) could also open new legitimate income sources for P2E.

Conclusion

Play to Earn stands at a crossroads. It disappointed as a short-term goldmine but has left its mark as an innovative concept. The challenge for a lawyer in the blockchain and gaming sector is to guide clients through this minefield toward concepts that are both worth playing and legally compliant. The chances for this are better if lessons are learned from phase one: transparency toward players, compliance with regulation, and safeguards against exploitation. If successful, the former bubble could evolve into an evolutionary model, meaningfully combining gaming and the real economy. Otherwise, Play to Earn will remain a cautionary tale of how quickly hype, greed, and legal uncertainty can implode.

Sources: The explanations refer to a variety of sources from the gaming community, legal literature, and official bodies. Selection (excerpt): Definition of P2E according to Chainlink; blockchain games Wikipedia; P2E market data and criticism (HackerNoon); Axie Infinity Case Study (taz, 2022); Ponzi analysis F5 Crypto; legal norms: Section 3 GlüStV 2021, KWG crypto value definition, BaFin leaflet; MiCAR classification (Bird&Bird); SEC/Howey application (Artaev Law); Dubai/VARA (CoinLedger) and many more. These and other references are cited in the text.